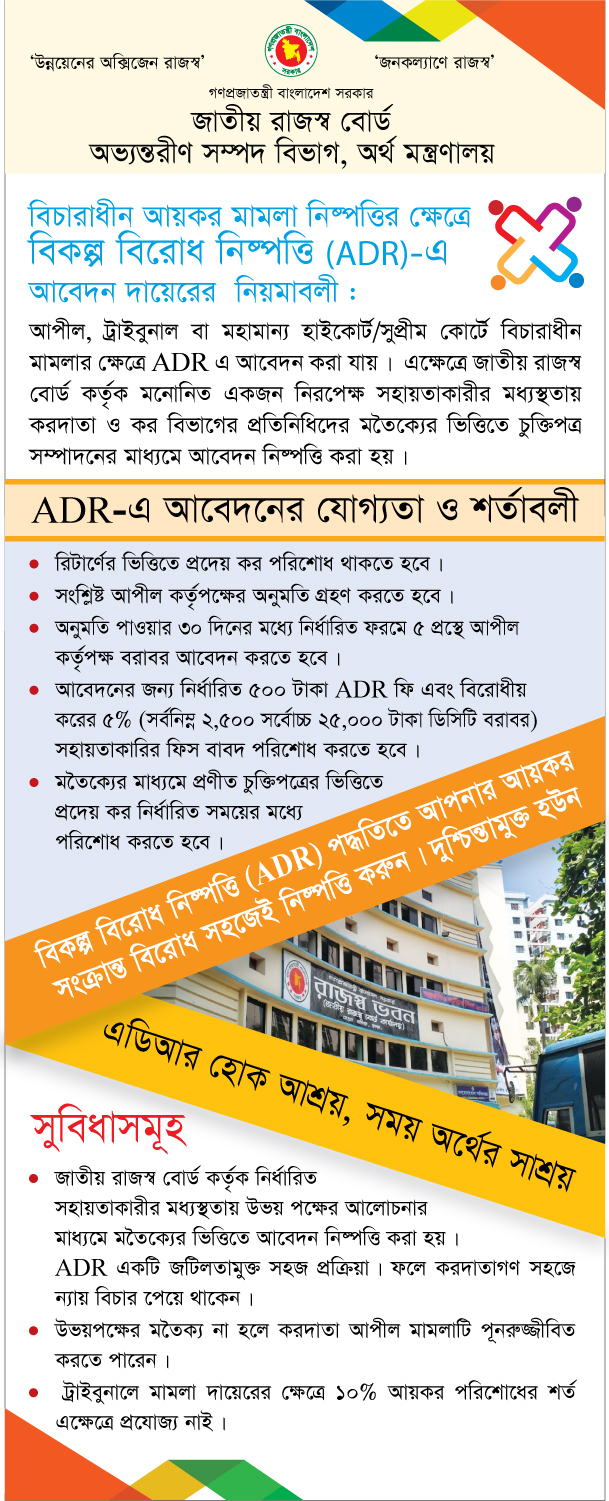

Alternate Dispute Resolution(ADR)

Alternate Dispute Resolution is a dispute litigation procedure outside the ordinary judicial and appeal system. Through ADR, disputes can be settled within the shortest possible time and cost. Thus, it is an optional dispute resolution procedure. Disputes are settled in ADR with a comprehensive and multipartite discussion under a congenial environment outside the purview of the court system. This helps to avoid/reduce the high cost of dispute settlement as compared to the conventional judicial system. The National Board of Revenue (NBR) as part of the Government is also benefited by quick conflict settlement and thus realizes the legitimate revenue. ADR has been popularized worldwide in Tax related fields. In line with this, Bangladesh has also induced ADR from FY 2011-12 in Customs, VAT and Income Tax related matters.

Disputes pending under Commissioner (Appeal), Customs, Excise and VAT Appellate Tribunal and High Court or Appeal Division of the Hon'ble Supreme Court can be resolved by ADR. National Board of Revenue has impartially published a pool of competent Facilitators for conducting ADR. Depending on their experiences in the specific field, the Commissionerate/ Appeal Commissionerate or the Appellate Tribunal can select one from them in order to facilitate a particular dispute. However, we should know that ADR is not arbitration. It just facilitates the parties to come to a gentlemen agreement by mutual understanding and respect. The agreement is jointly signed by both parties as well as the facilitator. Once the resolution is signed, both parties require following its terms and conditions. In ADR process, the VAT Commissioner nominates an officer to play a role on behalf of Government. Such an officer is termed as Departmental Representative by the ADR Rule. NBR prepared a list of Departmental Representative after concerning with the VAT Commissioners. This list if regularly updated.

To initiate a dispute settlement process, a written permission, from the authority under which the dispute is pending, is required. The taxpayer requires submitting a pay order as fee the amount of which depends on the value of the dispute. He also needs to submit a stamp worth of Tk. 500.00 as well as dispute related documents.

It is the unique feature of ADR that the taxpayer can return to the original judicial procedure in case there is no mutual settlement. Resolutions by ADR enjoy indemnity from any court proceedings. This means no challenges can be made against any decision made by ADR.

.jpg "National Board of Revenue (NBR), Bangladesh")